Economists say property prices might fall 10%. So What ?

Economists say property prices might fall 10%. So What ?

SOURCE: Australian Financial Review

With property prices up 400 per cent since 2000, what does a 10 per cent drop actually mean? And what happened the last time governments made major changes to property taxes?

Labor’s decision to introduce a minimum 30 per cent tax on capital gains from July 2027 and abolish negative gearing has rattled property investors. Auction clearance rates plunged below 50 per cent for the first time in eight years (excluding the pandemic era); home prices fell by 0.9 per cent in Sydney and 0.8 per cent in Melbourne, while Morgan Stanley now expects values to fall by up to 10 per cent in this downturn, which would be the largest property market correction in 40 years.

Not that Housing Minister Clare O’Neil took credit for the decline in prices, a central factor in improving housing affordability, when questioned by Channel seven's Natalie Barr on Wednesday. “The government’s changes, Nat, are not what’s driving house prices in our country principally,” O’Neil said.

Given Australian property prices have risen 400 per cent since 2000 and capital city markets are among the least affordable in the world, how bad could a 10 per cent price fall be? What happened the last time governments made significant changes to property taxes, and what do first home buyers make of it all?

What happened the last time Labor tried this?

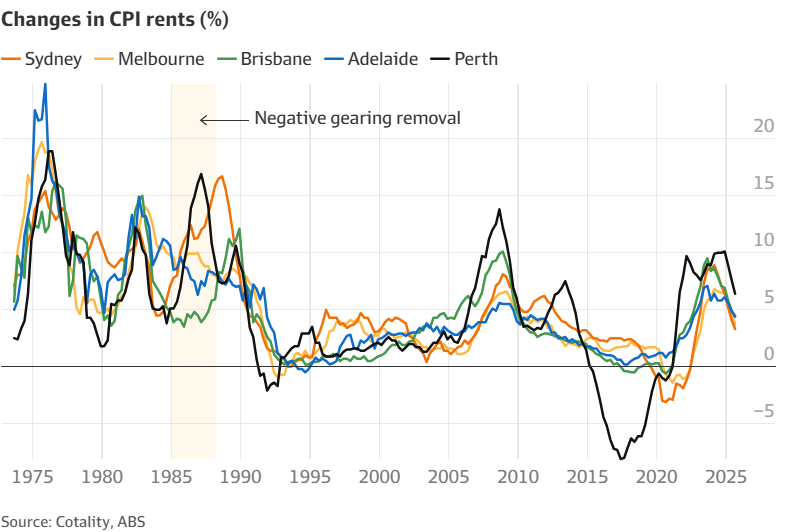

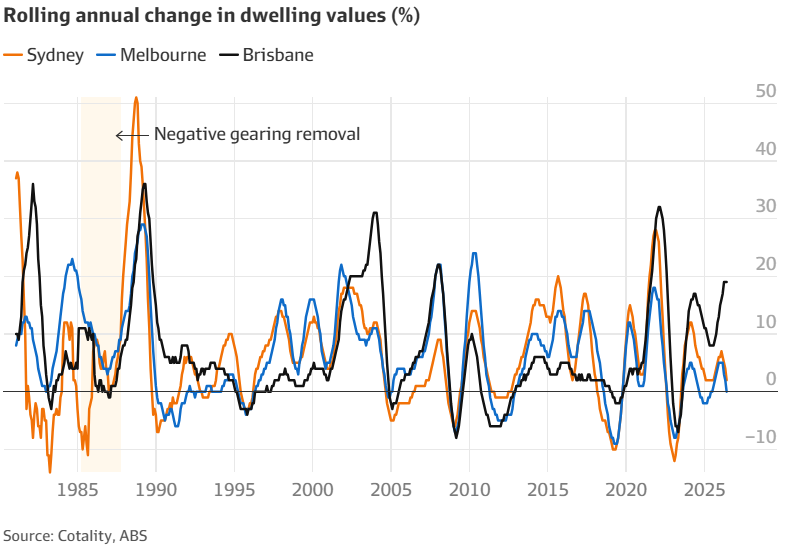

When the Hawke government removed negative gearing in July 1985, then-treasurer Paul Keating declared that the tax perk was “not adding to the stock of housing or to the stock of rental accommodation and failed to assist the families who actually needed it”.

Rents in Sydney and Perth spiked by about 30 per cent due to critically low vacancy rates, and the outcry meant negative gearing was restored two years later in September 1987.

Economists said the removal of negative gearing could not be blamed for the spike in rents, as the policy change had no effect in some markets.

“It just really highlights that there’s a lot more going on than just policy considerations here. It probably has a lot more to do with the underlying rental dynamics in these markets, particularly vacancy rates and the balance between rental demand and supply,” says Cotality’s research director Tim Lawless.

Independent economist Saul Eslake argues the 2026 budget tax changes will not cause rents to spike.

“Suppose it were true. Suppose that these changes prompt landlords to sell their properties en masse because we’re not getting negative gearing and CGT concession any more. Who would they sell them to? Well, not to other landlords ... but they would have to sell them to people who are looking to buy their own home,” Eslake says.

“While the supply of rental housing would fall, the demand for rental housing would fall by exactly the same amount. So, why should rents go up?”

On the contrary, Ray White chief economist Nerida Conisbee says renters will be worse off because while some will become first home buyers, there will always be more coming into the market.

“People leave home, they move from one city to another, they divorce, it doesn’t stop people becoming renters, and I think this is where the argument has really broken down,” Conisbee says.

“You end up in a situation where renters are still coming in, but there are not many new rental properties available, and as a result, rents start to rise.”

As for prices, over the 27 months that negative gearing was removed in the 1980s, Sydney prices rose 15 per cent, Melbourne prices were up 15.8 per cent and Brisbane 6.4 per cent.

When negative gearing was reinstated, prices boomed: Sydney values rose 44.2 per cent, Melbourne 32.8 per cent and Brisbane 52.8 per cent.

That boom also should not be blamed on the tax change. “It came after the 1987 sharemarket crash where a lot of investor demand is likely to have deflected towards real estate. There were also other structural drivers like financial deregulation and easier access to credit,” Lawless says.

A more recent example of removing negative gearing comes from across the ditch. In 2021, then-New Zealand prime minister Jacinda Ardern abolished mortgage interest deductibility – their equivalent to the property tax perk. However, by 2024, median rents had surged by nearly $100 a week, prompting the newly elected National Party prime minister, Christopher Luxon, to reinstate the investor tax concession.

Matt Nolan, research manager at the e61 Institute and a New Zealander, says it’s difficult to tie the rent rises to the tax policy.

“It ends up being quite hard to square things out, but there’s generally an impression among the people who advised on policy in places like Treasury, that nothing really happens to rents because of negative gearing, and it was a really marginal factor,” Nolan says.

So what does a 10pc fall in house prices actually mean?

A 10 per cent reduction in property prices takes us back to July 2024 prices for combined capitals. As chief economist at the Centre for Independent Studies Peter Tulip points out, we were having the same conversation about housing affordability then. So if not now, when?

The government has been quick to assert that the price reductions we’ve seen in the past few weeks are more to do with rising interest rates and uncertainty about the Middle East conflict than the budget changes.

“We should say house prices going down is the goal of good housing policy, especially in Australia, where house prices are so high,” says Jonathan O’Brien, lead organiser at housing think tank YIMBY Melbourne.

Lower prices and less competition from investors should allow more young Australians to buy their own homes. Tulip says this is most important for societal reasons rather than economic ones.

“There is a social cultural aspiration that we think it’s nice for young people to be able to buy a home,” he says.

But it goes beyond niceties. Eslake says people need to feel like they have a stake in the society and community they live in. Once they do, they feel more secure about having kids or starting a business.

Keeping the Australian dream of home ownership alive also helps to maintain social cohesion, housing research manager at the e61 Institute Nick Garvin says. If too many people start to feel like the system is rigged against them, they’re more likely to want to tear it all down.

These societal factors bleed into economic realities as well.

“If wealth is concentrated among fewer people, that wealth is less likely to translate through to consumption growth, and a lack of social cohesion can lead to political instability that leads to bad economic policies,” Garvin says.

But what do falling house prices mean for the economy?

It would dampen the “wealth effect” – the economic phenomenon where rising asset prices make home owners and investors feel wealthier and spend more, while falling prices trigger the reverse. While reduced spending would help tame inflation, it risks a broader economic slowdown, given that consumer spending is a primary driver of GDP.

The RBA estimates a 1 per cent increase in housing wealth translates into a 0.16 per cent increase in the long-run level of consumption. At this rate, Eslake says, the impact of a 10 per cent decrease in house prices would result in an “imperceptible” wealth effect.

But Trent Wiltshire, chief economist for Oceania at global construction consultancy Rider Levett Bucknall, says a 1.6 per cent decrease in long-run consumer spending, if property prices fall 10 per cent, combined with other factors would be “reasonably significant”.

“It affects real estate agents, lawyers, and conveyancers, banks, removalists. Then, when people move into a new home, they often renovate, buy new furniture, so it affects the construction sector as well, it affects the retail sector,” says Wiltshire.

What about ‘negative equity’? Is that a risk?

Falling house prices can create “negative equity” – where home buyers end up owing more than the asset is worth.

First home buyers who recently used the government’s 5 per cent deposit scheme are at greater risk of falling into negative equity because they have such a small stake in the home at the point of purchase (just 5 per cent) and have not paid off much of the loan to increase their holding.

A 5 per cent reduction in house prices would effectively erase the buyer’s equity (assuming they have just bought), a 10 per cent drop would mean many people on the scheme would owe more than their house is worth.

But economists are quick to dispel fears about this potential path. Tulip argues that most home owners in this situation are “still well ahead” and that “a 10 per cent fall in house prices is barely discernible in a long-term chart of what house prices have done”