Small in the Data, Critical in the Pipeline: Why SMSF Buyers Matter

The Federal Government's proposed ban on Self Managed Super Funds (SMSFs) borrowing to purchase residential property has been widely described as a relatively minor policy change. Based on official Australian Taxation Office (ATO) figures, new SMSF residential borrowing accounts for only a small proportion of the overall investment property market.

However, the real impact of this policy may not be reflected in the numbers alone.

The key question isn't how many properties SMSFs ultimately purchase. It's when they purchase them, and why that timing matters so much for Australia's housing supply.

Looking Beyond the Statistics

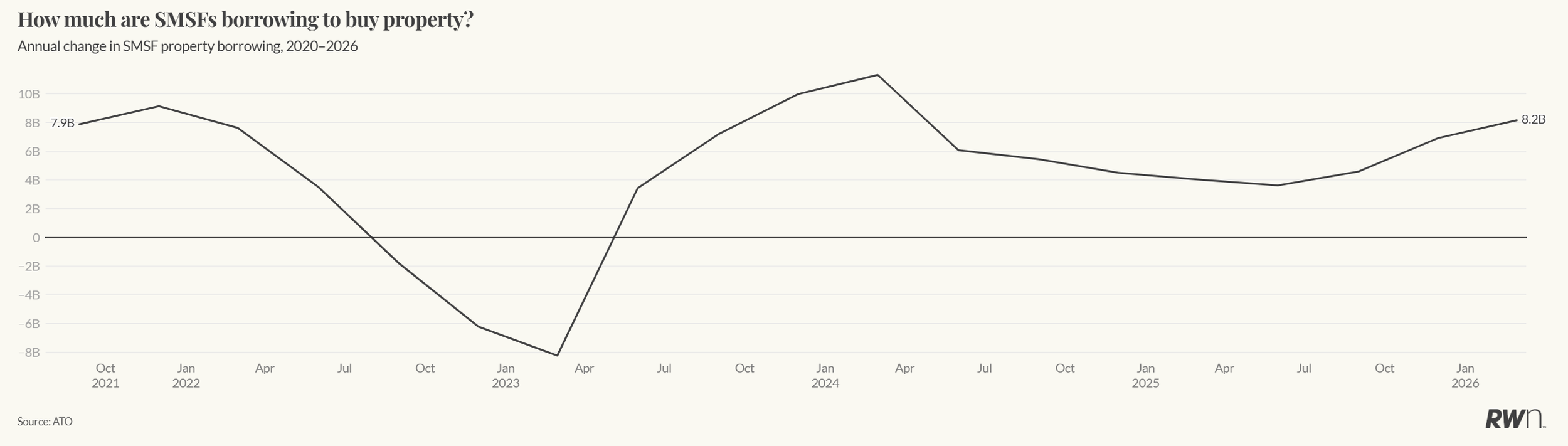

Treasury estimates that around 4,300 new Limited Recourse Borrowing Arrangements (LRBAs) were established by SMSFs for residential property in 2024, with an average of approximately 4,000 each year over the past eight years.

On paper, these figures suggest SMSF borrowing represents only a small slice of the property market.

Developers, however, tell a different story.

According to recent industry reports, several major property marketing and investment groups say they collectively facilitated more than 4,000 SMSF residential purchases in just the past year alone. The difference lies in where each side measures buyer activity.

The Importance of Pre Sales

Treasury's figures capture borrowing once it has been formally established and reported through tax data.

Developers, on the other hand, see SMSF buyers much earlier in the process.

An SMSF purchaser may sign a contract months, or even years, before construction is complete. These early commitments are often essential because they help developers achieve the pre sale targets required by banks before construction finance is approved.

Without enough committed buyers, many projects simply don't proceed.

This means the value of an SMSF buyer extends far beyond purchasing a single apartment or townhouse. Their commitment can help unlock funding for an entire development.

Why This Matters for Housing Supply

Australia's housing shortage is fundamentally a supply issue.

New homes are only built when developers can secure finance, and finance often depends on achieving sufficient pre sales.

If a group of buyers that regularly participates in this early stage is removed from the market, the consequences may be much larger than the official lending figures suggest.

Projects may be delayed.

Some developments may never commence.

Fewer homes ultimately reach the market.

This creates flow on effects for both owner occupiers and renters, particularly at a time when housing affordability and rental shortages remain major national challenges.

SMSF Buyers Fill an Important Niche

SMSF investors are not spread evenly across the housing market.

They are more commonly found purchasing:

New apartments

Townhouses

House and land packages

Investor focused developments

More affordable new housing options

These are also the types of developments where achieving pre sales can be particularly challenging when investor confidence weakens.

Removing SMSF borrowing reduces one of the buyer groups that often helps these projects reach the critical threshold needed to begin construction.

The Bigger Picture

While SMSF borrowing alone is unlikely to dramatically shift Australia's property market, its role within the development pipeline is far more significant than headline lending data suggests.

Every buyer who helps a project reach construction finance potentially contributes to dozens, or even hundreds, of new homes being built.

In a country striving to increase housing supply, policies that reduce early stage buyer demand may have unintended consequences that extend well beyond the relatively small number of SMSF loans recorded each year.

As Australia works towards delivering more housing, encouraging projects to move from planning to construction should remain a priority. Supporting the buyers who help make those developments possible may prove just as important as supporting the developers themselves.