What the SMSF Borrowing Ban Means for Property Investors

The Federal Government has officially passed legislation banning Self Managed Super Funds (SMSFs) from borrowing to purchase residential property.

While the announcement has attracted plenty of attention, the reality is that most property investors won't be immediately affected. However, if you're considering using your superannuation to invest in residential real estate, it's important to understand exactly what has changed and what it means for the future.

What's Changing?

Under the new legislation, SMSFs will no longer be able to borrow money to purchase residential property.

The ban takes effect 45 days after the legislation receives Royal Assent.

Importantly, existing SMSF residential property loans are protected. If your fund already owns residential property under a Limited Recourse Borrowing Arrangement (LRBA), nothing changes.

The legislation also does not affect commercial property purchases through an SMSF. Trustees can continue to borrow for eligible commercial property investments under the existing rules.

Understanding SMSF Property Borrowing

When an SMSF purchases property using borrowed funds, it does so through a Limited Recourse Borrowing Arrangement, commonly known as an LRBA.

This structure allows an SMSF to use its existing superannuation balance as a deposit while borrowing the remaining funds to complete the purchase.

The "limited recourse" feature means that if the loan defaults, the lender's claim is limited to the property itself. The SMSF's other investments remain protected.

For many Australians, this provided an opportunity to build long term wealth through residential property while keeping the investment inside their superannuation.

It is this borrowing option for residential property that has now been removed.

Why Has the Government Introduced the Ban?

Concerns about SMSF borrowing have existed for more than a decade.

The 2014 Murray Financial System Inquiry recommended restricting the practice due to potential financial stability risks. Similar recommendations were later made by the Council of Financial Regulators in both 2019 and 2022.

The proposal remained dormant until this year's broader tax reforms.

With changes to negative gearing and capital gains tax, SMSFs were increasingly viewed as one of the remaining tax effective ways to invest in residential property using borrowed funds.

The Government has now closed that pathway for future residential property purchases.

How Much of the Property Market Is Actually Affected?

Despite the media attention, SMSF borrowing represents only a relatively small portion of Australia's overall property market.

According to the latest Australian Taxation Office data:

SMSFs hold more than $1 trillion in total assets.

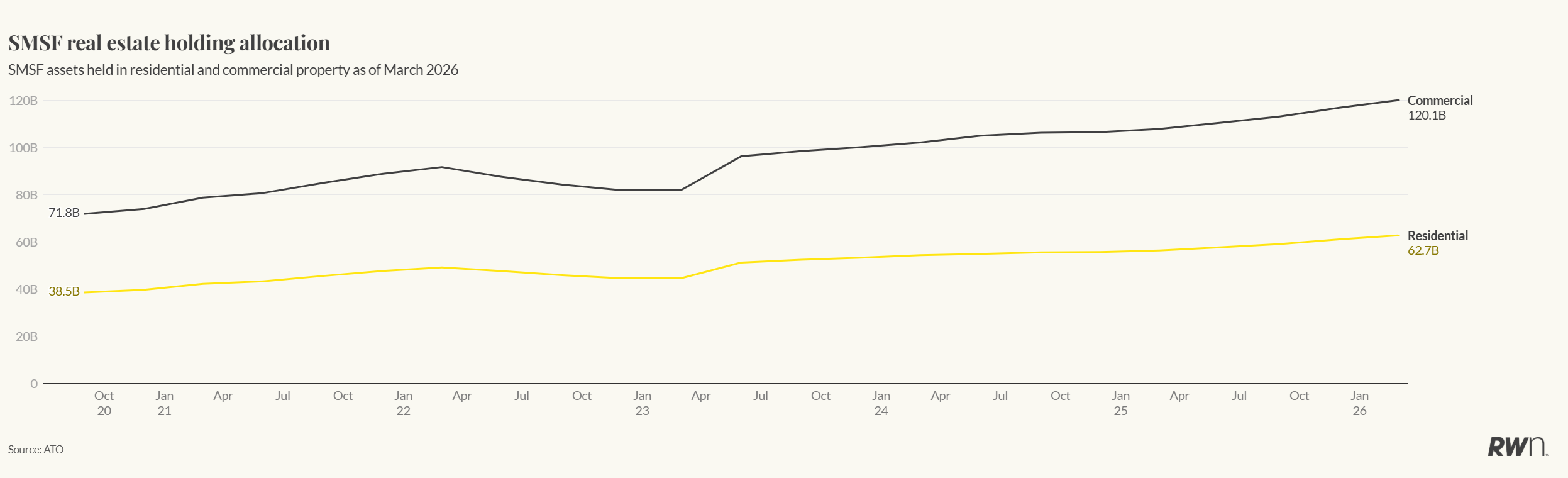

Residential property accounts for approximately $62.7 billion of those holdings.

Commercial property holdings total around $120.1 billion and remain unaffected.

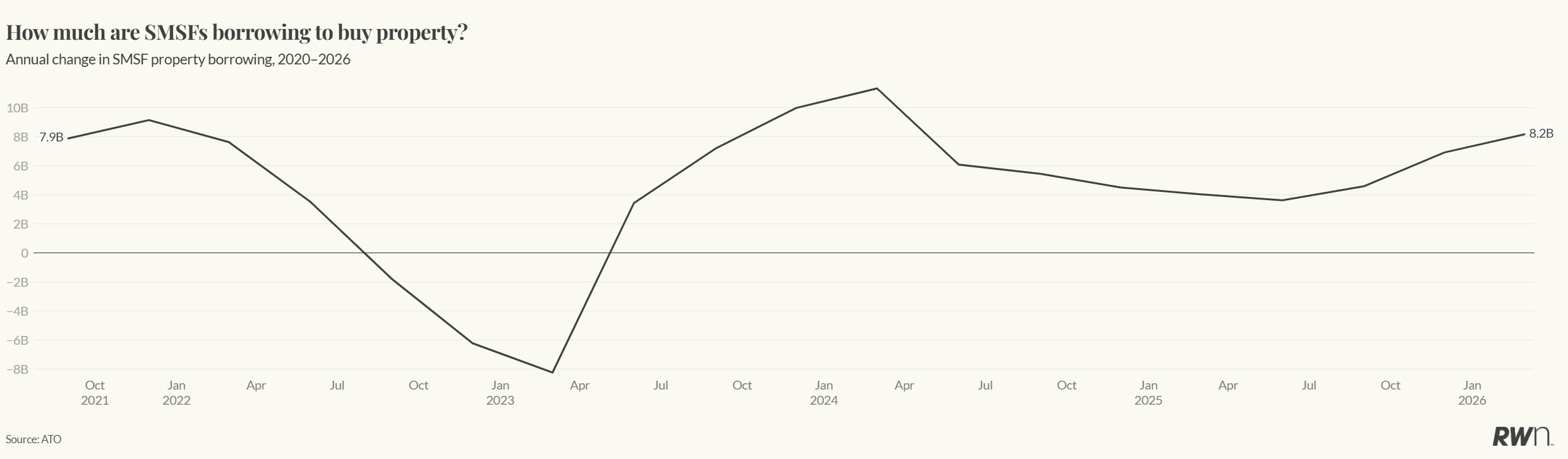

National investor lending significantly outweighs annual SMSF residential borrowing.

While the direct market impact may be relatively modest, the changes will affect investors who were planning to use their superannuation to purchase residential property in the future.

What Does This Mean for Existing SMSF Investors?

If you already own residential property within your SMSF, you can breathe easy.

Your existing borrowing arrangements remain fully protected under the new legislation.

The only change applies to future residential property purchases using borrowed funds inside an SMSF.

There is also a 45 day transition period after Royal Assent, allowing transactions already underway sufficient time to be completed before the new rules begin.

What Should Investors Do Now?

If you've been considering purchasing residential property through your SMSF using finance, time is now an important factor.

Those with transactions already in progress should speak with their financial adviser, lender and solicitor to ensure they understand the transition arrangements and key deadlines.

For investors planning future property purchases, it may be worth exploring alternative investment strategies, whether inside or outside superannuation.

The Bottom Line

For most Australians, this legislation won't change their current investment strategy.

However, it does remove one of the few remaining opportunities to borrow within superannuation to purchase residential property.

While existing investors are protected, future buyers will need to consider different pathways to build wealth through property.

As with any major legislative change, obtaining advice from a qualified financial adviser or SMSF specialist is the best way to understand how the new rules may affect your individual circumstances.