Will Property Prices Crash? Why First Home Buyer Markets Could Feel the Biggest Impact

There's been growing talk about a property market crash across Australia.

Auction clearance rates have softened, buyer confidence has cooled and recent Federal Government policy changes have created fresh uncertainty in an already cautious market.

But while the headlines may suggest a nationwide downturn, the reality is likely to be far more complex.

Rather than seeing prices fall everywhere, we're more likely to see some parts of the market outperform while others come under greater pressure.

A National Crash Still Looks Unlikely

Despite recent concerns, several key factors continue to support Australia's housing market.

Housing supply remains well below demand.

Population growth continues to place pressure on available housing.

Construction costs remain high and the delivery of new homes is still constrained.

These factors make a widespread collapse in property prices unlikely.

Instead, market performance is expected to vary significantly depending on location and buyer type.

Why First Home Buyer Markets Are More Vulnerable

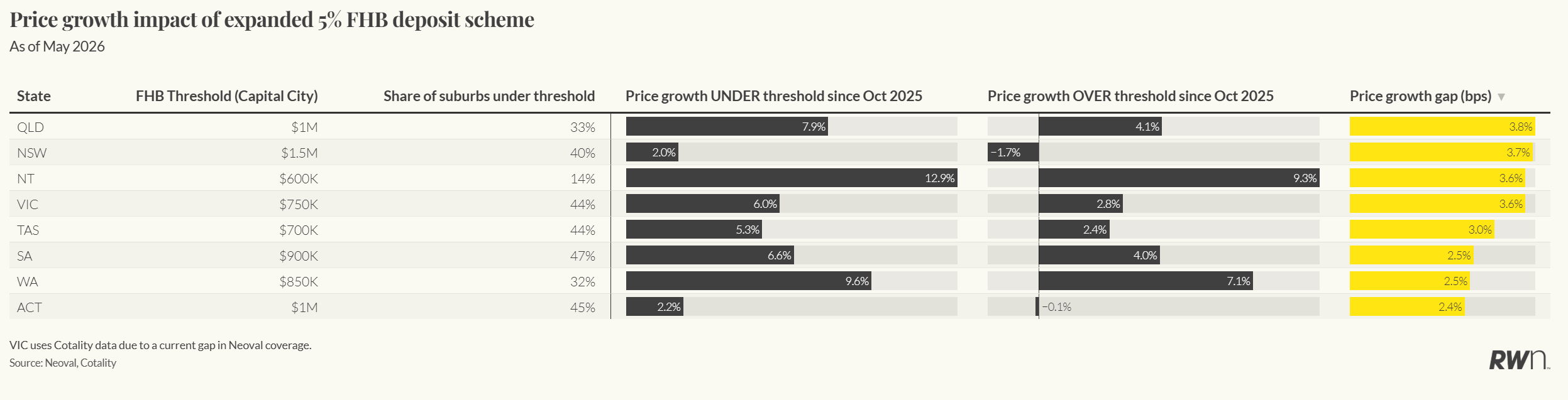

The areas facing the greatest risk are lower priced suburbs that have benefited most from government incentives aimed at helping first home buyers.

Since expanding the 5 per cent deposit scheme in October 2025, the Government removed income limits, increased property price caps and made the program available without place limits.

This dramatically increased purchasing power for eligible first home buyers.

Because the scheme only applied to homes below certain price thresholds, demand became concentrated in more affordable suburbs rather than being spread evenly across the market.

Government Support Helped Drive Price Growth

Recent lending data showed a noticeable increase in first home buyer activity following the expansion of the scheme.

As more buyers entered the market, prices in eligible suburbs generally grew faster than those in higher priced areas.

Across several states, suburbs that qualified under the scheme consistently outperformed markets above the price thresholds.

This wasn't simply the result of stronger market conditions. It was largely driven by targeted government policy.

The Market Is Now Entering a New Phase

While first home buyer incentives boosted demand, recent Federal Budget changes are expected to reduce investor activity, particularly in the more affordable end of the market.

This matters because investors and first home buyers often compete for the same types of properties, including:

Apartments

Townhouses

Entry level houses

Affordable investment properties

If investor demand begins to weaken, these markets may lose one of the key drivers that has supported price growth over the past year.

Higher Priced Markets May Hold Up Better

Premium suburbs have generally been less affected by first home buyer incentives and are also less exposed to changes impacting investors.

As a result, higher value markets may prove more resilient if buyer demand softens.

Rather than a broad market correction, Australia could see a widening gap between different market segments.

What This Means for First Home Buyers

For buyers who entered the market using a 5 per cent deposit, there is an added consideration.

With relatively small equity buffers, even modest price declines could temporarily place some homeowners into negative equity, where the value of the property falls below the remaining loan balance.

This doesn't necessarily create financial hardship if homeowners continue making repayments and don't need to sell.

However, it does reduce flexibility and increases financial risk if circumstances change.

The Bottom Line

The current property market is being influenced by several factors at once, including interest rates, government policy changes, global economic uncertainty and shifting buyer confidence.

While these conditions are creating a softer market, they do not point to a nationwide property crash.

Instead, Australia is likely to experience a more uneven market.

The suburbs that benefited most from first home buyer incentives may now face greater pressure as investor demand slows, while higher priced markets could prove more resilient.

For buyers, sellers and investors alike, understanding these local market differences will be far more important than focusing solely on national headlines.